Industry News

SELECTED ITEMS OF INTEREST TO THE MEDIA COMMUNITY

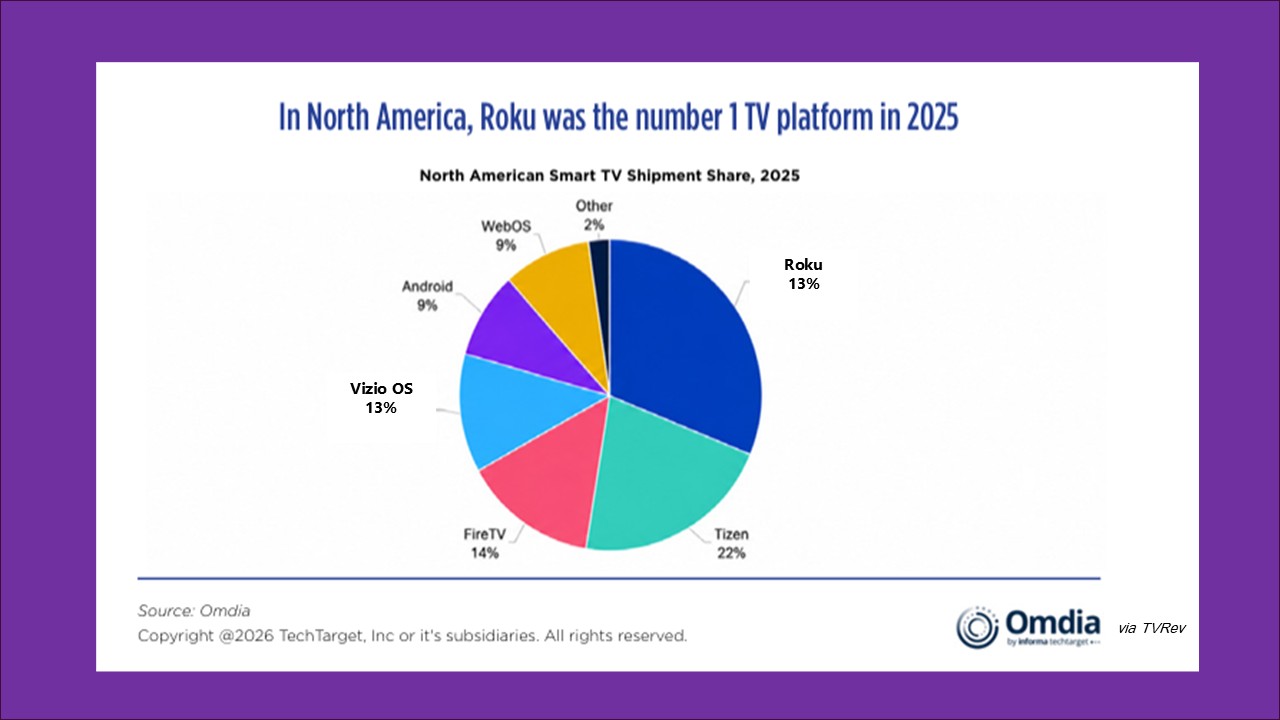

TV Operating Systems: Putting a lock on all of it through discovery leverage, monetization control, and data

It has been a 15-year long slow build, but the TV operating system is increasingly important as cable distribution is becoming increasingly irrelevant. TVRev's newly published round-up and analysis of TV operating systems – the software layer that runs the smart TV – and their histories gives an excellent blow-by-blow narrative. The TV OS Wars, written by Alan Wolk, is a thorough discussion of the players and issues facing “the entire television experience.” The write-up is appropriately long and nuanced, with a decent go at identifying “what's next."

Wolk explains why the TV OS is the “ultimate controller.” Here are just a few excellent nuggets of analysis:

- It’s first come, first served. “The TV OS matters because it does not merely organize the user’s experience. It prioritizes the various components of it.”

- It’s the software. “The old television gatekeepers controlled access through distribution. The new ones control it through the interface. And in a world where viewers are faced with an endless supply of content, controlling the interface is the power move.”

- It’s the data. “The digital nature of streaming means that unlike broadcast TV, TV operating systems are able to collect a range of data on viewer behavior, data that is valuable to advertisers and programmers alike.”

- “It’s an ad platform for brands who realize that the minutes when viewers are deciding what to watch is prime ad space because of its prominence and because it is not interrupting the viewing experience.”

- It is “TV OS’s secret weapon. That’s because it creates the sort of monetization that allows manufacturers to make money in a world of razor thin margins.”

Besides explaining why this matters, the report also gives a lot of detail about who the TV manufacturers and the OS suppliers are – and a good run at market share information.

Read the full report by clicking on the link to receive a download.

#managementconsulting #mediaconsulting #streaming

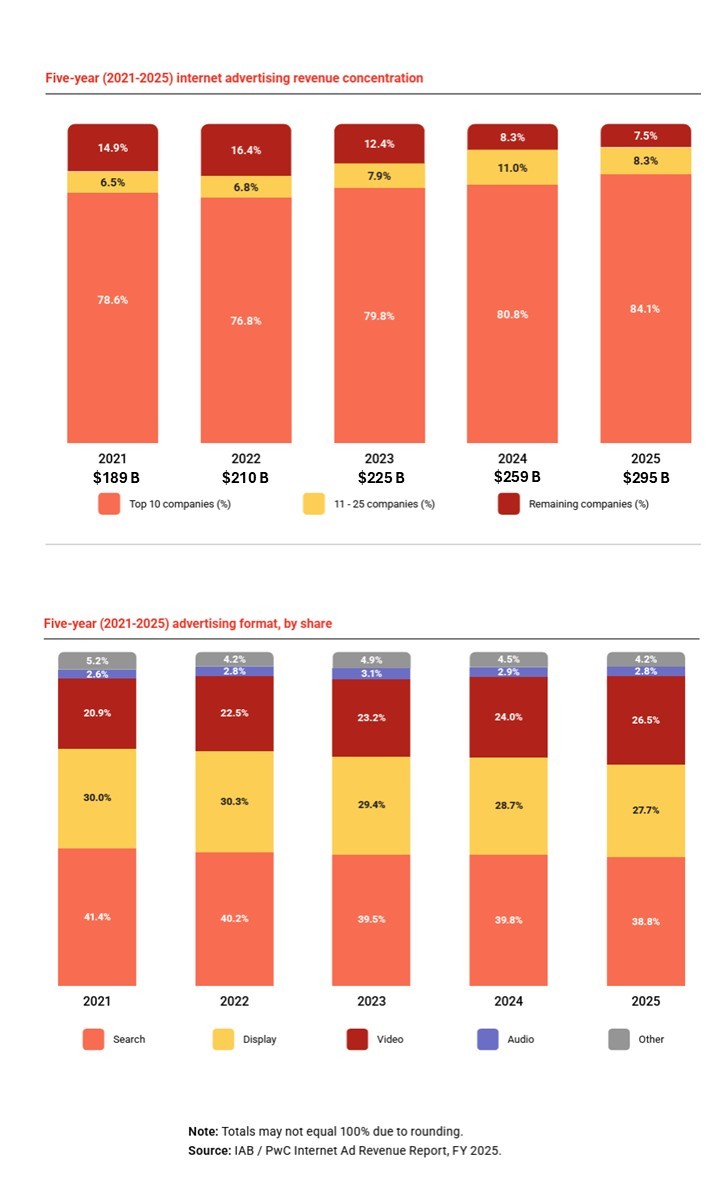

The Big Get Bigger, the Formats Shift: Two Charts That Explain the Last 5 Years of Digital Advertising

Even as digital advertising in the U.S. has increased 12% per year from 2021 to 2025, the industry is consolidating and the popularity of rich media is where advertisers are spending their dollars. Two charts from the PWC/IAB report, Internet Advertising Revenue Report, Full-year 2025 results, concisely shows these trends.

“The Internet revenue concentration” chart sketches out the marked increased of industry concentration, since “The Top 10” grow from 81% of the total revenue in 2024 to 84% in 2025. Clearly, advertisers are migrating away from independent publishers and smaller ad networks to the big guys because of the ease of use in advertising on them; and the results must be better, or they wouldn't be there. They are also the keeper of the keys for AI. IAB states that AI has transitioned from an optional feature into the "infrastructure layer through which discovery, commerce, and media execution operate."

Although, the report does not explicitly name individual corporations, the tech giants take up 6 of those spots:

- Alphabet (Google & YouTube)

- Meta (Facebook & Instagram):

- Amazon (their commerce network for both search, display and video)

- Microsoft (including LinkedIn & Bing)

- ByteDance (TikTok):

- Apple

“The Advertising format by share” chart tracks the structural evolution of digital layouts, showing a steady reallocation of spending away from static text-based formats of Search and Display towards rich, dynamic media of Video and Audio. Although Search maintains the largest absolute share of the ecosystem, its growth momentum has decelerated.

Read the full report.

#digitaladvertising #managementconsulting #digitalmarketing

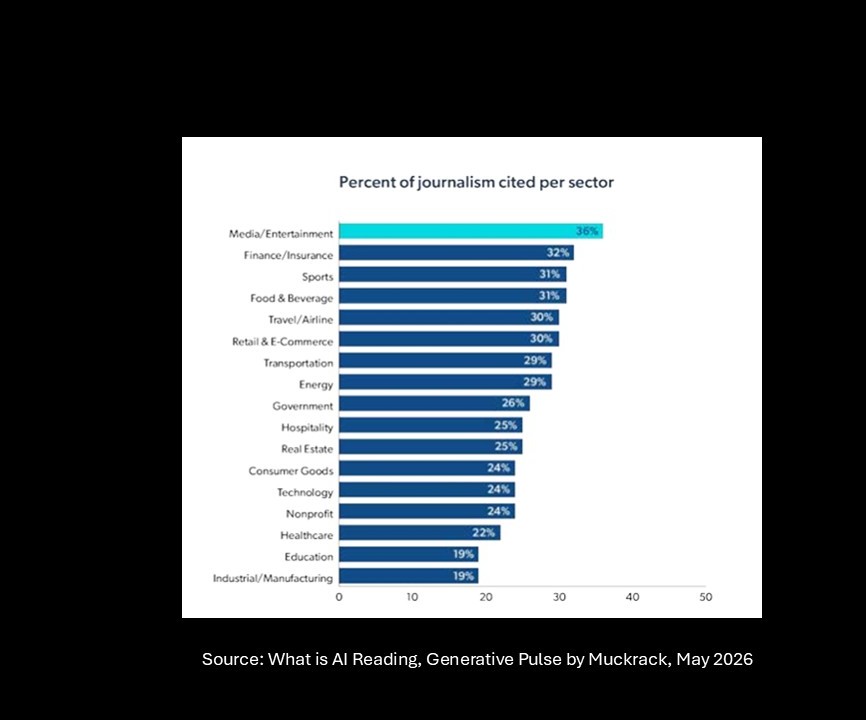

What in the world is AI reading? And does it let you know?

The Generative Pulse, published by Muckrack, examined over 25 million links from AI prompts to compile which sources were cited and for which industries and products. Published in May 2026, Generative Pulse compared the prompt results from the three AI providers: ChatGPT (OpenAI), Claude (Anthropic), and Gemini (Google.) Although the report warns that the behaviors observed will shift as the models are retrained, the differences in this snapshot are pronounced and makes you think. The information is meant to give some guidance to companies in a variety of industries looking to impact consumers.

Top Take-aways in the study:

- “Journalism and earned media remain the foundation of AI citations." About 99% of links cited by AI come from non-paid sources. Journalism accounts for about 27% of all citations.

- “AI providers have distinct citation habits.” ChatGPT cites sources in 96% of responses, averaging 5 citations per response; Claude note specific citations in 55% of responses, averaging 13 citations. Gemini cites sources in 82% of responses with an average of 8 citations.

- “Some industries lean on journalistic content more than others.” Media/Entertainment leads all sectors with 36% of queries citing journalism and manufacturing at 19% the lowest.

Read the study. #mediaconsulting #managementconsulting #contentstrategy #AICitations